Private Mortgage Insurance, or PMI, can be cancelled in three different ways; Automatic Cancellation, Early Cancellation based on Original Value, or Early Cancellation based on Current Value.

In this article, we will discuss these three options in detail including eligibility requirements, required Loan-to-Value ratio, and whether an option is right for you.

In the options below, your loan is required to reach a certain Loan to Value ratio or LTV. LTV compares your outstanding mortgage balance with the value of your property. When you purchase a home, the value of your property will always be the lower of the purchase price and the appraised value of your property. LTV can be calculated using the following formula: (Loan Balance/Property Value)*100 = LTV

Automatic Cancellation

For single family primary residences, PMI will automatically be cancelled at a pre-determined date when the loan is scheduled to reach 78% LTV. For this to occur, your mortgage must be current at the time of the scheduled cancellation. If you default on your loan, you may still be eligible for cancellation but not until your loan reinstates.

There are no additional fees or documentation required for automatic cancellation of PMI and in most cases, no action is required on your part.

Early Cancellation Based on Original Property Value

To be eligible for this option, your mortgage must reflect an acceptable payment record, which means:

- The mortgage payment for the month preceding the date of the cancellation request is paid

- No payments 30 or more days past due in the last 12 months

- No payments 60 or more days past due in the last 24 months

Additionally, your LTV must be at or below a certain threshold before PMI is waived. The required LTV will vary by property type. For Single Family Principal Residences, an LTV of 80% or less is required. For Multi-Family or Investment properties, a lower LTV is required. Contact the UHM Customer Care team for more information.

This requirement may be achieved by continuing to make your mortgage payment until your loan reaches the required LTV or sending a larger payment to reduce the principal balance to 80% LTV.

Finally, in some cases. a new property valuation must reflect that the current property value is at least equal to the original property value.

Early Cancellation Based on Current Property Value

To be eligible for this option, your mortgage must reflect an acceptable payment record, which means:

- The mortgage payment for the month preceding the date of the cancellation request is paid.

- No payments 30 or more days past due in the last 12

- No payments 60 or more days past due in the last 24

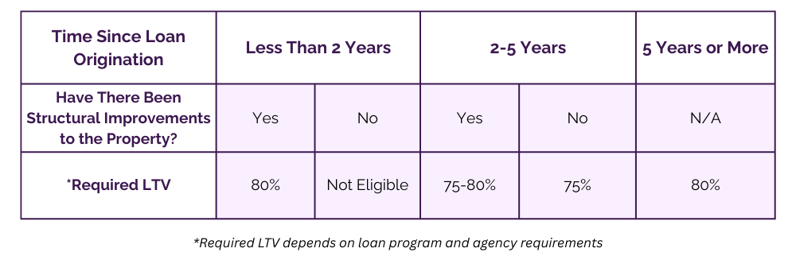

Additionally, a new property valuation must reflect the required LTV based on the type of property and age of your mortgage as follows:

For Single Family Primary Residences

For all Multi-Family or Investment properties your mortgage must be at least 24 months old or have structural improvements completed. Additionally, a lower LTV is required. Contact the UHM Customer Care team for more information.

Structural Improvements are anything that significantly improves the longevity of your property. Examples include replacing the roof with improved materials, updating siding, updating electrical, replacing windows, increasing interior livable square footage, etc.

Structural Improvements are not the same as cosmetic improvements such as repainting interior walls a different color, replacing appliances, or landscaping the exterior of the property.

For more information on what PMI is, check out our article What is PMI and Why do I need it?

For more information on cancelling PMI based on the options above, please contact the UHM Customer Care Team at 800-441-3456 or email pmi@uhm.com

For more information on Refinancing your loan to remove PMI, please contact a UHM Loan Officer today at 1-877-846-4968 or Find Loan Officer with the link below.

Related Resources

Need Mortgage Guidance?

We’ve got the answers you’re looking for.